General Requirements (takes about 5-minutes or less to apply online)

680 FICO score (Transunion or Experian FICO model 8.0 or similar) [down from 700]

Less than -15% operating loss in the last year of business

Last 2-Years of filed Business Tax Returns; Last 1-Year of filed Personal Tax Returns

Last 3-months of bank statements; copy of Driver’s License

U.S. Small Business Administration Lowers FICO Score Requirements for Business Loan Applicants

The U.S. Small Business Administration (SBA) is an independent federal agency established in 1953 dedicated to aiding, counseling, assisting, and protecting the interests of small businesses, helping them start, grow, expand, or recover.

As of April 6th, 2025, the SBA has relaxed its requirements for minimum FICO score from 700 down to an adjusted 680.

In this brief, we will go over the best ways to gain approval for an SBA loan where payback terms (amortizations) can be 10-years, or even 25-years, significantly reducing cash flow necessary to meet business debt service payments.

Read about how to best gain approval with the U.S. Small Business Administration through its originating banks and partners.

Navigating the Path to SBA Financing: A Business Owner's Guide to Loan Qualification

The U.S. Small Business Administration (SBA) plays a pivotal role in fostering the growth and resilience of America's small business sector.

A key component of its mandate involves facilitating access to capital through government-guaranteed loan programs.

These programs aim to bridge financing gaps, enabling businesses to start, expand, and navigate economic challenges.

This white paper provides a comprehensive guide for business owners seeking to understand and qualify for SBA financing, based exclusively on information sourced from the official sba.gov website.

It details the SBA's mission in relation to lending, outlines the primary loan programs available—namely the 7(a), 504, and Microloan programs—and examines their specific eligibility requirements concerning business size, fund usage, creditworthiness, owner equity, and collateral.

The analysis highlights foundational eligibility pillars common across programs, such as operating a for-profit entity within the United States, meeting specific size standards, demonstrating creditworthiness, and establishing a need for government-backed financing.

Furthermore, the paper emphasizes the critical importance of thorough preparation, including the development of a robust business plan and accurate financial statements, and underscores the necessity of collaborating effectively with SBA-approved lending partners (banks, Certified Development Companies, or Microloan intermediaries).

By synthesizing eligibility criteria and success factors identified through sba.gov resources, this report presents a clear, actionable roadmap designed to equip business owners with the knowledge needed to strategically position themselves for SBA loan qualification.

General Requirements (takes about 5-minutes or less to apply online)

680 FICO score (Transunion or Experian FICO model 8.0 or similar) [down from 700]

Less than -15% operating loss in the last year of business

Last 2-Years of filed Business Tax Returns; Last 1-Year of filed Personal Tax Returns

Last 3-months of bank statements; copy of Driver’s License

Leveraging SBA Support for Your Business Growth

The objective of this white paper is to furnish small business owners and entrepreneurs with a clear, reliable, and actionable guide to understanding the SBA loan landscape and navigating the qualification process.

The information presented herein is drawn exclusively from resources available on the official sba.gov website, as reflected in the provided source materials.

The scope of this analysis centers on the three primary SBA loan programs designed for general business financing: the 7(a) Loan Program, the 504 Loan Program, and the Microloan Program.

It will delve into the specific eligibility criteria associated with each program, including requirements related to business size, permissible uses of loan proceeds, credit standards, owner equity contributions, and collateral.

Furthermore, this paper will examine factors identified on sba.gov that tend to strengthen a loan application, outline the typical steps involved in the application process, and discuss common reasons for loan denial along with strategies to mitigate those risks.

While the SBA offers other valuable funding options such as disaster assistance loans, surety bonds, grants, and investment capital programs like SBICs , this document maintains a focused scope on the core loan programs most frequently sought by businesses for startup and expansion capital.

Key SBA Loan Programs: The SBA's Role Guaranteeing Loans, Reducing Risk

A fundamental aspect of the SBA's approach to business financing is its role as a guarantor, rather than a direct lender, for most of its loan programs.

With the specific exception of disaster loans provided directly to affected businesses and homeowners, the SBA does not typically issue funds straight to small business borrowers.

Instead, the agency partners with a network of approved lending institutions—including banks, credit unions, and specialized financial entities—by setting the guidelines under which loans are made and providing a government guarantee for a significant portion of each loan.

This guarantee mechanism is the cornerstone of the SBA's ability to expand capital access.

By reducing the financial risk borne by the lending partners, the SBA makes these institutions more willing and able to extend credit to small businesses.

This is particularly beneficial for businesses that may possess sound operational plans and potential but might not fully meet conventional, stricter lending criteria, perhaps due to limited operating history, insufficient collateral, or being in a perceived higher-risk industry.

The SBA guarantee effectively bridges this gap, facilitating funding access that might otherwise be unavailable.

Consequently, the relationship between the business owner and the lender becomes paramount, as the lender conducts the primary underwriting and makes the ultimate credit decision, albeit operating within the SBA's established framework and with the security of the SBA's partial guarantee.

The benefits for small businesses accessing SBA-guaranteed loans, as highlighted on sba.gov, can be significant. These often include competitive terms, with interest rates and fees generally comparable to those of non-guaranteed loans.

Additionally, SBA-backed loans may offer unique advantages such as lower down payment requirements, more flexible considerations regarding overhead expenses, and, in some specific loan types or circumstances, the possibility of securing financing without providing collateral.

Furthermore, certain SBA loan programs are coupled with ongoing counseling and educational support, providing valuable resources to help entrepreneurs successfully start and manage their businesses.

General Requirements (takes about 5-minutes or less to apply online)

680 FICO score (Transunion or Experian FICO model 8.0 or similar) [down from 700]

Less than -15% operating loss in the last year of business

Last 2-Years of filed Business Tax Returns; Last 1-Year of filed Personal Tax Returns

Last 3-months of bank statements; copy of Driver’s License

Overview of Major SBA Loan Programs

The SBA offers a portfolio of loan programs designed to meet diverse business needs. Based on information from sba.gov, the three primary programs providing general-purpose financing are the 7(a) Loan Program, the 504 Loan Program, and the Microloan Program. Understanding the distinct purpose and structure of each is a critical first step for any business owner considering SBA financing.

7(a) Loan Program: This is characterized as the SBA's "primary" and most versatile loan program. 7(a) loans offer broad flexibility in how the funds can be used, encompassing needs such as acquiring real estate, purchasing equipment, financing working capital, refinancing existing debt, and even funding business acquisitions (changes of ownership). These loans are delivered through SBA-approved 7(a) lenders, typically banks and credit unions.

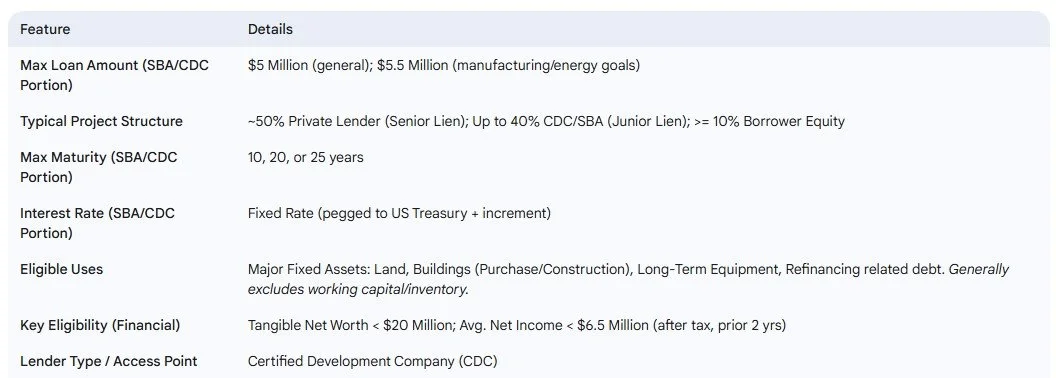

504 Loan Program: In contrast to the flexibility of the 7(a), the 504 program provides long-term, fixed-rate financing specifically targeted towards the acquisition or development of major fixed assets. Eligible uses focus on assets that promote business growth and job creation, such as purchasing land and buildings, constructing facilities, or buying heavy machinery and equipment. A unique feature of the 504 program is its delivery mechanism: loans are made in partnership between a conventional lender, the small business borrower, and a Certified Development Company (CDC)—a nonprofit, community-based entity certified and regulated by the SBA to promote local economic development.

Microloan Program: This program addresses the need for smaller amounts of capital, offering loans up to $50,000, with the average loan size being considerably smaller (around $13,000). Microloans are designed to support startups and the expansion of existing small businesses, as well as certain non-profit childcare centers. Funds can be used for purposes like working capital, inventory, supplies, furniture, or equipment. Similar to the 504 program's reliance on CDCs, Microloans are not obtained directly from banks but rather through specially designated intermediary lenders—typically nonprofit, community-based organizations with expertise in lending and providing technical assistance to small businesses.

The existence of these distinct programs signifies the SBA's recognition that small businesses face varied capital requirements at different stages and for different purposes. A business needing flexible working capital would likely look to the 7(a) program, while one planning a major facility expansion would be better served by the 504 program's structure and fixed rates.

A startup needing a small injection of funds for initial inventory might find the Microloan program most appropriate. Attempting to secure financing through the wrong program (e.g., seeking general working capital via a 504 loan) would result in ineligibility. Therefore, accurately identifying the business's specific funding need and aligning it with the correct SBA program is a crucial preliminary step before engaging with potential lenders.

While this paper focuses on these three core programs, business owners should be aware that the SBA offers other specialized financing options mentioned on sba.gov.

These include programs tailored for exporters (Export Express, Export Working Capital, International Trade Loans under the 7(a) umbrella), specific working capital solutions (CAPLines, also under 7(a)), direct loans for disaster recovery (Physical Damage Loans, Economic Injury Disaster Loans), and loans for businesses impacted by military deployments (Military Reservist Loan).

Foundational Eligibility: Meeting SBA's Core Requirements

Across its major loan programs (7(a), 504, Microloan), the SBA establishes several fundamental eligibility requirements that businesses must meet before specific program criteria are even considered. These foundational standards act as initial gateways to SBA financing.

A. Basic Business Structure and Location

A primary requirement is that the applicant business must operate on a for-profit basis. This generally excludes non-profit organizations from eligibility for standard business loans, although the Microloan program documentation specifically notes an exception allowing certain non-profit childcare centers to qualify. Furthermore, the 504 program explicitly prohibits loans to businesses engaged in passive or speculative activities, reinforcing the focus on active, operational enterprises.

Secondly, the business must be physically located and operate within the United States or its possessions and territories. This geographic limitation ensures that SBA resources support domestic economic activity.

Thirdly, the applicant must be an operating business. This implies the entity is actively engaged in commerce or providing services, rather than existing solely for investment purposes or speculative ventures, which are generally ineligible.

B. Defining "Small": SBA Size Standards

A critical and non-negotiable requirement across SBA loan programs is that the applicant business must qualify as "small" according to the SBA's official size standards. These standards vary by industry, typically defined using the North American Industry Classification System (NAICS) code, and are usually based on metrics such as the average number of employees or average annual receipts over a specific period.

It is important to note that the provided source materials consistently reference the requirement to meet these size standards but do not contain the detailed tables or the online Size Standards Tool necessary to perform the assessment.

Therefore, this white paper must emphasize that determining size eligibility is a mandatory step requiring business owners to consult the sba.gov website directly or work closely with an SBA lender, CDC, intermediary, or an SBA Resource Partner (like an SBDC).

Failing to meet the applicable size standard for the intended loan program renders a business ineligible, regardless of other qualifications. This underscores the importance of verifying size status early in the process to avoid investing time and resources in an application that cannot proceed.

C. Creditworthiness and Repayment Ability

While the SBA guarantee mitigates risk for lenders, it does not absolve the borrower from demonstrating financial responsibility.

Eligibility hinges on the business being deemed creditworthy and possessing the demonstrable ability to repay the loan.

Lenders evaluate this through a comprehensive assessment of the business's financial health, including its credit history , existing debt structure, projected cash flows, and overall financial condition.

The standard, as stated on sba.gov, is that the business's credit must be "sound enough to assure loan repayment".

Interestingly, sba.gov suggests that even businesses with "bad credit" may still qualify for startup funding. This indicates potential flexibility, perhaps through specific programs or lenders willing to consider mitigating circumstances or compensating factors.

Microloan intermediaries, for instance, establish their own specific lending and credit requirements , which might differ from traditional bank standards.

However, the overarching principle remains: a strong credit profile and clear evidence of repayment capacity significantly strengthen an application.

Lenders ultimately provide the definitive list of credit and eligibility requirements for the specific loan product.

The government guarantee serves to make viable, yet perhaps marginally unqualified by conventional standards, deals possible; it is not intended to subsidize businesses lacking fundamental financial soundness or a realistic path to repayment.

Therefore, potential applicants must prioritize strengthening their financial position and presenting compelling evidence of future repayment ability through well-supported business plans and financial projections.

D. Demonstrating Need: The "Credit Elsewhere" Test

A unique aspect of SBA loan eligibility is the "credit elsewhere" test. Businesses seeking SBA-guaranteed loans must demonstrate that they have been unable to obtain the requested financing on reasonable terms from non-Federal, non-State, or non-local government sources.

This requirement reinforces the SBA's intended role: to fill a gap in the private lending market, rather than competing with or replacing conventional financing options.

This test does not necessarily mandate that a business must have received formal loan denials from multiple conventional lenders. Instead, it focuses on whether comparable credit is available from private sources without the need for a government guarantee, under terms considered "reasonable" for the business's situation. The lender assisting the business with the SBA application plays a key role in evaluating and documenting whether this criterion is met. The consistent inclusion of this test across program descriptions highlights its importance in targeting SBA resources effectively to businesses that genuinely require this form of support to access needed capital. Business owners should be prepared to articulate why conventional financing options are not suitably available or viable for their specific needs on comparable terms.

E. Eligible Business Types

Finally, sba.gov states that certain types of businesses are inherently ineligible for its loan programs. While the provided materials do not offer an exhaustive list of ineligible industries or activities, specific exclusions are mentioned.

For example, the 504 loan program explicitly excludes businesses primarily engaged in non-profit, passive (like holding property for investment income), or speculative activities.

Given these restrictions, it is crucial for business owners to verify with their potential lender or an SBA representative early in the process that their specific type of business and the intended use of funds align with SBA eligibility guidelines.

General Requirements (takes about 5-minutes or less to apply online)

680 FICO score (Transunion or Experian FICO model 8.0 or similar) [down from 700]

Less than -15% operating loss in the last year of business

Last 2-Years of filed Business Tax Returns; Last 1-Year of filed Personal Tax Returns

Last 3-months of bank statements; copy of Driver’s License

The 7(a) Program: SBA's Flagship

The 7(a) loan program stands as the SBA's most common and flexible financing tool, designed to meet a wide spectrum of small business needs.

Eligibility & Uses: Businesses must meet the general eligibility criteria previously discussed (for-profit, US-based, size standards, credit elsewhere test). The program's hallmark is its versatility in fund usage. Proceeds from a 7(a) loan can be applied to:

Acquiring commercial real estate (land and buildings)

Refinancing existing mortgages or improving real estate/buildings

Funding short-term or long-term working capital needs

Refinancing existing business debt (under certain conditions)

Purchasing and installing machinery, equipment, furniture, fixtures, and supplies

Financing Artificial Intelligence (AI)-related expenses

Funding changes of ownership (acquiring another business), either partially or fully

Loan Amounts, Terms, Rates, Fees:

Loan Amount: The maximum loan amount for most 7(a) loans is $5 million. However, certain sub-programs within the 7(a) family, such as SBA Express and Export Express, have lower maximums, typically $500,000. The SBA's maximum guaranteed exposure on a standard 7(a) loan is generally $3.75 million, though it can be higher for specific programs like International Trade loans.

Guaranty Percentage: The portion of the loan guaranteed by the SBA varies. For standard 7(a) loans, the guarantee is typically up to 85% for loans of $150,000 or less, and up to 75% for loans exceeding $150,000. This percentage can differ for sub-programs: SBA Express carries a 50% guarantee , while export-focused programs like Export Express and Export Working Capital may offer guarantees up to 90% to mitigate international risk.

Loan Maturity: Loan terms are determined based on the use of proceeds and the borrower's ability to repay, aiming for the shortest appropriate term. Generally, the maximum maturity is 10 years for working capital or equipment financing (unless the equipment has a documented useful life exceeding 10 years). For real estate acquisition or improvement, the maximum term can extend up to 25 years. Revolving lines of credit offered under certain 7(a) sub-programs have shorter maximum terms, such as up to 10 years for SBA Express , 36 months or less for Export Working Capital , or 60 months for the 7(a) Working Capital Pilot (WCP) program.

Interest Rates: Rates are negotiated between the borrower and the lender but are subject to SBA-established maximums. These maximums are typically pegged to a benchmark rate like the Prime Rate, plus a permissible spread that varies depending on the loan amount and maturity. For instance, variable-rate loans might have maximums ranging from Prime + 6.5% for loans $50,000 or less, down to Prime + 3.0% for loans greater than $350,000. Rates can be either fixed or variable. Notably, the Export Working Capital Program (EWCP) does not have an SBA-imposed maximum interest rate limit.

Fees: Lenders are required to pay the SBA an upfront Guaranty Fee for each 7(a) loan; this fee can be passed on to the borrower. Lenders also pay an ongoing Annual Service Fee based on the guaranteed portion's outstanding balance, which cannot be charged to the borrower. The specific amounts for these fees are published annually by the SBA. Additionally, prepayment penalties may apply to 7(a) loans with maturities of 15 years or longer if the borrower voluntarily prepays 25% or more of the outstanding balance within the first three years of disbursement.

Collateral: SBA's collateral requirements for 7(a) loans are nuanced and depend significantly on the loan size and specific sub-program:

For loans of $50,000 or less under programs like 7(a) Small and SBA Express, the SBA generally does not require lenders to take collateral (an exception exists for International Trade loans).

For SBA Express loans over $50,000, lenders may use their existing collateral policies but are instructed not to decline a loan solely due to inadequate collateral.

For 7(a) Small loans between $50,001 and $500,000, lenders are expected to follow their established internal collateral policies used for similarly-sized, non-SBA guaranteed commercial loans.

For Standard 7(a) loans (typically over $500,000), the SBA expects the loan to be "fully secured." This generally means the lender takes security interests in all assets being acquired, refinanced, or improved with the loan proceeds, plus any other available fixed assets of the business, up to the loan amount. Specific details are outlined in SBA's Standard Operating Procedures (SOPs).

Sub-Programs: The flexibility of the 7(a) program is further enhanced by several specialized delivery methods or sub-programs tailored to specific needs. Key variants mentioned in sba.gov resources include :

Standard 7(a): Generally refers to loans over $500,000 that don't fall into other specific categories.

7(a) Small: Loans up to $500,000, potentially with streamlined processing.

SBA Express: Loans up to $500,000 with an accelerated SBA response time and a lower guarantee percentage (50%). Lenders use their own forms and procedures more extensively and make the credit decision. Offers revolving lines of credit up to 10 years.

Export Express, Export Working Capital (EWCP), International Trade: Programs designed to support businesses engaged in international trade, offering features like higher guarantee percentages (up to 90%) and specific uses related to export development or financing export transactions.

CAPLines: An umbrella program providing lines of credit to help businesses meet short-term and cyclical working capital needs. Includes specific lines for seasonal needs, contract financing, and builders.

Working Capital Pilot (WCP) Program: A pilot program offering monitored lines of credit up to $5 million, combining features of existing lines of credit to support growing businesses, particularly those in manufacturing, wholesale, or services with strong financial reporting capabilities.

The inherent flexibility that makes the 7(a) program attractive also introduces complexity.

The array of sub-programs, each with potentially different terms, guarantee levels, collateral rules, and even processing methods (e.g., lender credit decisions in SBA Express), means that a "one-size-fits-all" approach is inadequate.

Successfully navigating the 7(a) landscape requires careful consideration of the business's specific needs and close collaboration with an experienced SBA lender who can help identify the most suitable sub-program and guide the application process accordingly.

SBA 7(a) Loan Program Snapshot

Understanding the 504 Program: Financing Growth Assets

The SBA 504 loan program offers a distinct financing structure specifically designed for businesses undertaking major fixed asset projects that foster business growth and create jobs.

Eligibility & Uses: Applicants must meet the general SBA eligibility standards (for-profit, US-based, size standards, repayment ability, good character, qualified management, feasible business plan). Additionally, the 504 program has specific financial thresholds: the business must have a tangible net worth of less than $20 million and an average net income of less than $6.5 million after federal income taxes for the two years preceding the application. (Note: Earlier documentation cited lower thresholds of $15M net worth and $5M net income , but the figures $20M/$6.5M appear in more recent updates ).

The use of 504 loan proceeds is strictly limited to financing major fixed assets. Eligible projects include:

Purchasing land and constructing new buildings

Buying existing buildings and/or making improvements

Acquiring long-term machinery and equipment

Improving or modernizing land, streets, utilities, parking lots, and landscaping associated with a facility project

Refinancing existing debt that meets specific criteria related to fixed asset financing ("qualified debt").

Crucially, 504 funds generally cannot be used for working capital, inventory, or consolidating/repaying debt unrelated to fixed assets. A specific allowance for financing AI-related working capital, intellectual property, or consulting "soft costs" associated with a larger project is noted in recent documentation, representing a potential exception.

Structure & Role of CDC: The 504 program operates through a unique partnership structure involving three parties: the small business, a conventional third-party lender (typically a bank), and a Certified Development Company (CDC). CDCs are non-profit organizations certified and regulated by the SBA to promote economic development within their communities. A typical 504 project financing structure involves:

The third-party lender provides a loan covering approximately 50% of the total project cost, secured by a senior lien on the assets.

The CDC provides a loan covering up to 40% of the project cost, secured by a junior lien. This CDC portion is funded through an SBA-guaranteed debenture (a type of bond sold to private investors).

The small business borrower contributes an equity injection of at least 10% of the project cost. (Note: Specific percentages are standard practice but not explicitly detailed in the provided snippets, though the partnership model and CDC role are clear). This structure makes the program accessible by reducing the required down payment from the business owner compared to many conventional loans. Businesses must work directly with a CDC to access the 504 program; applications are not made directly to banks for the SBA-guaranteed portion. CDCs possess specialized knowledge of 504 regulations and guide businesses through the process.

Loan Amounts, Terms, Rates:

Loan Amount (CDC/SBA Portion): The maximum amount for the CDC loan portion (backed by the SBA guarantee) is generally $5 million. This can increase to $5.5 million for projects meeting specific public policy goals, such as those related to manufacturing or energy efficiency.

Loan Maturity: The CDC/SBA portion of the loan offers long repayment terms, with 10-, 20-, or 25-year maturity options available. This long amortization period helps keep monthly payments manageable.

Interest Rates: A key advantage of the 504 program is the interest rate on the CDC/SBA portion. It is a fixed rate for the entire life of the loan, providing long-term payment stability. The rate is pegged to an increment above the current market rate for 10-year U.S. Treasury issues at the time the debenture funding the loan is sold. This often results in favorable, below-market fixed rates compared to conventional long-term financing.

The specific focus on fixed assets, the partnership structure involving CDCs, and the availability of long-term, fixed interest rates define the 504 program's niche.

It is an ideal financing tool for established businesses planning significant investments in property or equipment that will support long-term growth and job creation.

The stability offered by the fixed rate is particularly advantageous for long-range financial planning.

However, its strict limitations on the use of funds make it unsuitable for businesses primarily seeking working capital or inventory financing.

Accessing the program requires identifying and collaborating with a local CDC.

SBA 504 Loan Program Snapshot

General Requirements (takes about 5-minutes or less to apply online)

680 FICO score (Transunion or Experian FICO model 8.0 or similar) [down from 700]

Less than -15% operating loss in the last year of business

Last 2-Years of filed Business Tax Returns; Last 1-Year of filed Personal Tax Returns

Last 3-months of bank statements; copy of Driver’s License

Leveraging the Microloan Program: Accessible Small-Scale Funding

For businesses needing smaller amounts of capital, the SBA Microloan program offers a targeted solution, distinct from the larger 7(a) and 504 programs.

Eligibility & Uses: This program provides loans up to a maximum of $50,000, although the average loan size is significantly smaller, around $13,000. It is designed to assist small businesses, including startups, with expansion needs. Notably, it also extends eligibility to certain not-for-profit childcare centers.

Eligible uses for microloan funds are focused on supporting operational growth and include:

Working capital

Purchase of inventory or supplies

Acquisition of furniture or fixtures

Purchase of machinery or equipment

Microloans generally cannot be used to repay existing debts or to purchase real estate (inferred from the list of eligible uses).

Role of Intermediaries: A defining characteristic of the Microloan program is its delivery mechanism. The SBA does not lend these funds directly, nor are they typically accessed through banks participating in the 7(a) program. Instead, the SBA provides funding to a national network of designated intermediary lenders. These intermediaries are usually nonprofit, community-based organizations with specific experience in micro-lending and providing business management and technical assistance. The intermediary organization makes the loan directly to the small business borrower.

Crucially, each intermediary lender establishes its own specific lending and credit requirements. While general SBA eligibility guidelines apply, the intermediary determines the precise credit standards, application process, and collateral requirements. sba.gov notes that intermediaries generally require some form of collateral and often a personal guarantee from the business owner. This localized control allows intermediaries to potentially serve businesses or communities that might face challenges accessing traditional bank financing.

Loan Amounts, Terms, Rates:

Loan Amount: Up to $50,000.

Loan Maturity: Repayment terms vary based on the loan amount, the planned use of funds, the specific intermediary's requirements, and the needs of the borrower. However, the absolute maximum repayment term allowed for an SBA microloan is seven years.

Interest Rates: Interest rates also vary depending on the specific intermediary lender. sba.gov indicates that rates generally fall between 8% and 13%

Finding Intermediaries: To apply for a microloan, a business owner must identify and work directly with an SBA-approved intermediary serving their geographic area. Information on locating these intermediaries is available through SBA resources, likely including a searchable list on the sba.gov website.

The Microloan program serves as a vital resource for entrepreneurs needing modest capital injections, whether for starting a new venture or funding a small expansion.

It can be particularly valuable for businesses that may not qualify for larger traditional bank loans or 7(a) loans, or whose funding needs simply fall below typical bank minimums.

Success in obtaining a microloan hinges on building a relationship with the local intermediary lender and meeting their specific requirements, which may emphasize community impact or character alongside traditional financial metrics.

SBA Microloan Program Snapshot

Positioning for Approval: Key Success Factors

Securing an SBA-guaranteed loan involves more than just meeting the basic eligibility criteria. Lenders (and the SBA) assess the overall viability and potential of the business. Based on sba.gov resources, several factors significantly strengthen a loan application and increase the likelihood of approval.

A. The Cornerstone: A Viable Business Plan

While explicitly mentioned as a general eligibility standard for the 504 program , a comprehensive and feasible business plan is implicitly essential for all SBA loan applications. It serves as the primary document for articulating the business's value proposition, market analysis, operational strategy, management team qualifications, and, critically, how the requested loan funds will be utilized to achieve specific, measurable goals. A well-crafted business plan is indispensable for demonstrating to a lender that the business has a sound purpose , a clear path to profitability, and the capacity to generate sufficient cash flow to meet its repayment obligations.

B. Presenting Strong Financials

Accurate, organized, and realistic financial information is paramount. Lenders scrutinize historical financial performance (for existing businesses) and future projections to gauge the business's health and repayment ability. The requirement for participants in the 7(a) WCP pilot program to produce timely financial statements, accounts receivable/payable aging reports, and inventory reports highlights the importance lenders place on robust financial tracking and transparency. A strong application package typically includes:

Historical financial statements (Profit & Loss, Balance Sheet, Cash Flow Statement) for the past few years, if applicable.

Detailed, well-supported financial projections (Profit & Loss, Balance Sheet, Cash Flow Statement) for the next several years, clearly outlining the assumptions used.

Personal financial statements for all principal owners of the business.

C. Demonstrating Management Capability

Lenders invest in people as much as they invest in ideas. The 504 program explicitly lists qualified management expertise as a general eligibility standard , and this principle holds true across all loan programs. Lenders need confidence in the ability of the business owners and key managers to execute the business plan successfully. Demonstrating relevant industry experience, a track record of accomplishments, strong leadership skills, and a well-defined organizational structure can significantly bolster an application.

D. Owner Equity Injection

While specific minimum equity injection percentages are not detailed for all programs in the provided snippets (though the 504 structure implies at least 10% from the borrower), the concept of "owner's equity" or "skin in the game" is a fundamental principle in lending. Lenders generally expect business owners to contribute a reasonable amount of their own capital to the venture or project being financed. This personal investment demonstrates commitment, aligns the owner's interests with the lender's, and provides a cushion against unforeseen challenges. The required amount can vary depending on the loan program, the nature of the business (startup vs. existing), the total project cost, and the lender's specific policies. Prospective borrowers should be prepared to discuss their planned equity contribution with the lender.

E. Meeting Collateral Requirements (Where Applicable)

As discussed previously, collateral requirements differ significantly across SBA loan programs and loan sizes. While some smaller loans or specific programs like SBA Express may have minimal or no formal collateral requirements imposed by the SBA , many larger loans, particularly Standard 7(a) and those from Microloan intermediaries, will necessitate securing the debt with assets. These assets can include business assets being purchased with loan funds (equipment, real estate) or existing business assets (accounts receivable, inventory, machinery). In some cases, personal assets of the owners might also be required as collateral. Business owners should proactively identify potential collateral, understand the specific requirements of the loan program they are pursuing, and be prepared to pledge available assets. It's also worth noting the flexibility mentioned for SBA Express, where a loan cannot be declined solely based on inadequate collateral , suggesting that other strengths might compensate in some situations.

F. Utilizing SBA's Support Network

Perhaps one of the most valuable, yet potentially underutilized, resources for prospective borrowers is the SBA's extensive network of Resource Partners. These organizations offer free or low-cost counseling, training, and technical assistance designed to help small businesses start, grow, and succeed—including navigating the complexities of loan applications. Engaging with these partners can significantly enhance a business owner's preparedness and the overall quality of their loan package. Key Resource Partners highlighted in sba.gov materials include:

Small Business Development Centers (SBDCs): With a nationwide network of over 900 locations, SBDCs provide in-depth management and technical assistance, helping businesses tackle financial, marketing, operational, and planning challenges.

SCORE: This nonprofit organization leverages a vast network of volunteer business executives (current and retired) to provide free, confidential mentoring and workshops based on real-world experience.

Women's Business Centers (WBCs): Focused on empowering women entrepreneurs, WBCs offer comprehensive training, counseling, and access to resources, particularly supporting those who are economically or socially disadvantaged.

(Implied) Veterans Business Outreach Centers (VBOCs): While not detailed, the mention of preserving staffing within the Office of Veterans Business Development suggests dedicated support structures exist for veteran entrepreneurs.

In addition to these partners, SBA District Offices serve as local points of contact for information and assistance.

Proactively leveraging these support systems is not a sign of weakness but a strategic move.

These partners can provide invaluable guidance in developing a robust business plan, refining financial projections, understanding lender expectations, and ensuring the loan application is complete and compelling.

This preparatory support directly addresses many common weaknesses that can lead to loan denial, thereby increasing the chances of a successful outcome.

The SBA Loan Application Journey

Securing an SBA-guaranteed loan follows a structured process, although specific steps may vary slightly depending on the loan program and the lender involved. Understanding this typical pathway can help business owners navigate the process more effectively.

A. Step 1: Preparation is Paramount

Before approaching any lender, thorough preparation is essential. This involves:

Gathering Documentation: Assemble key documents required for most business loan applications. This typically includes a comprehensive business plan, historical financial statements for existing businesses (usually 2-3 years), detailed financial projections (profit & loss, cash flow, balance sheet), personal financial statements for all owners with significant stakes, copies of business licenses and registrations, and potentially business and personal tax returns. The need for a "feasible business plan" and accurate financial reporting underscores the importance of these documents.

Refining Plans and Projections: Critically review and refine the business plan and financial projections for clarity, realism, and internal consistency. Ensure assumptions are well-documented and justifiable. Consider seeking assistance from SBA Resource Partners (SBDCs, SCORE, WBCs) during this stage to strengthen the package.

Determining Needs and Program Fit: Clearly define the specific amount of funding required and how the funds will be used. Based on this need, identify the most appropriate SBA loan program (7(a), 504, or Microloan) by comparing their eligible uses, loan amounts, and terms.

B. Step 2: Finding the Right Lending Partner

A crucial point to remember is that, except for disaster loans, SBA loan applications are submitted directly to the lending institution, not to the SBA itself. The type of institution to approach depends directly on the chosen loan program:

For 7(a) Loans: Businesses should seek out SBA-approved 7(a) lenders, which are typically banks or credit unions. SBA provides the Lender Match tool on its website (sba.gov) as a resource to help connect borrowers with participating lenders based on their needs and location.

For 504 Loans: The 504 program requires businesses to work through a Certified Development Company (CDC). Businesses must identify and contact a CDC that serves their geographic area. The sba.gov website offers resources to help locate authorized CDCs. Approaching a bank directly for the SBA-guaranteed portion of a 504 loan is not the correct procedure; the CDC serves as the primary point of contact and facilitator for the SBA component.

For Microloans: Applications for microloans must be made through an SBA-approved intermediary lender. These are typically local, nonprofit community development organizations. Businesses need to identify the appropriate intermediary serving their area, likely using lists or search tools provided on sba.gov.

Using the correct channel is vital. Attempting to apply for a 504 loan directly at a bank branch without involving a CDC, or seeking a microloan from a standard 7(a) lender, will likely be inefficient and unsuccessful. Utilizing the resources provided by SBA (Lender Match, CDC finders, intermediary lists) ensures engagement with the appropriate institutions authorized to handle the specific loan program.

C. Step 3: Compiling the Application Package

Once a suitable lending partner (Lender, CDC, or Intermediary) is identified, the business owner will work with that institution to complete the formal application package. This involves:

Filling out the specific application forms required by the lending institution and potentially the SBA.

Submitting all the supporting documentation gathered during the preparation phase (business plan, financials, etc.).

Providing any additional information requested by the lender during their underwriting process.

The exact contents of the application package can vary depending on the loan type, the requested loan amount, and the lender's specific processing methods (e.g., streamlined processes for SBA Express). For 7(a) loans, SBA Form 1919 (Borrower Information Form) is generally required, although lenders, particularly those using the SBA Express method, may primarily rely on their own forms and procedures. The lender, CDC, or intermediary will guide the applicant on the specific requirements.

D. Step 4: Lender Review and SBA Guarantee Process

After receiving the complete application package, the lending partner conducts its underwriting review. This involves assessing the business's eligibility, creditworthiness, repayment ability, collateral (if applicable), and the overall feasibility of the request. The lender, CDC, or intermediary makes the primary credit decision.

If the lending institution approves the loan subject to receiving an SBA guarantee, it then submits the necessary documentation and analysis to the SBA for review (unless the lender has been granted "delegated authority" by the SBA, which allows them to process, close, and service the loan without prior SBA review, common in programs like SBA Express). The SBA reviews the lender's submission to ensure the loan complies with its program requirements and eligibility standards. SBA's turnaround time for this review can vary; for Standard 7(a) loans, it is cited as typically being 5-10 business days.

E. Step 5: Closing and Funding

Once the SBA approves the guarantee (or if SBA review is not required due to delegated authority) and all loan conditions set by the lender and SBA have been met, the loan can proceed to closing. The lender finalizes the loan documents, which are then signed by the business owner(s). Following closing, the loan funds are disbursed according to the agreed-upon schedule and purposes outlined in the loan agreement.

After funding, the borrower begins making regular payments (typically monthly principal and interest) directly to the lender for 7(a) loans or potentially through a Central Servicing Agent for 504 loans. For certain loans that may have been purchased by the SBA (e.g., defaulted loans), borrowers might utilize the MySBA Loan Portal (lending.sba.gov) to monitor their loan status and potentially make payments.

General Requirements (takes about 5-minutes or less to apply online)

680 FICO score (Transunion or Experian FICO model 8.0 or similar) [down from 700]

Less than -15% operating loss in the last year of business

Last 2-Years of filed Business Tax Returns; Last 1-Year of filed Personal Tax Returns

Last 3-months of bank statements; copy of Driver’s License

VII. Proactive Measures: Mitigating Loan Denial Risks

While SBA loan programs are designed to expand access to capital, applications can still be denied. Understanding common reasons for denial allows business owners to take proactive steps to mitigate these risks before and during the application process.

A. Addressing Credit Issues Proactively

A weak credit history or low credit score is a frequent obstacle. Although sba.gov suggests that "bad credit" might not be an absolute barrier for some startup funding , lenders fundamentally need assurance of repayment.

Mitigation: Before applying, business owners should obtain and review both their personal and business credit reports. Identify and dispute any errors. Work to resolve outstanding collections, judgments, or liens. Develop a clear, honest explanation for any past credit problems and present a plan for responsible financial management going forward. Discussing these issues transparently with the potential lender early on is often better than letting them discover problems independently.

B. Strengthening Repayment Capacity Evidence

Lenders must be convinced that the business can generate sufficient cash flow to cover the loan payments along with its other obligations. Insufficient projected cash flow or weak evidence supporting those projections is a major reason for denial.

Mitigation: Develop realistic, well-researched financial projections. Back up revenue forecasts with solid market data, customer contracts, or letters of intent where possible. Ensure expense projections are comprehensive and reasonable. Clearly articulate the key assumptions behind the numbers. Engaging SBA Resource Partners (SBDCs, SCORE) can provide expert assistance in developing credible and compelling financial projections.

C. Navigating Collateral Shortfalls

While some SBA programs offer flexibility , a lack of sufficient collateral to secure the loan can still be a challenge, particularly for larger loan amounts or under certain programs.

Mitigation: Conduct a thorough inventory of all available business assets (equipment, real estate, accounts receivable, inventory) and potentially personal assets that could be pledged as collateral. Understand the specific collateral expectations for the target loan program. Discuss the collateral position openly with the lender. If a shortfall exists, highlight other strengths of the application, such as strong cash flow, significant owner equity injection, or extensive management experience, which might partially compensate. Explore loan programs known for greater collateral flexibility, like SBA Express for amounts under $50,000.

D. Ensuring Application Completeness and Accuracy

An application package that is incomplete, contains errors, or lacks necessary documentation will inevitably lead to delays and potential denial.

Mitigation: Pay meticulous attention to detail when completing all application forms. Gather all required supporting documents well in advance. Double-check figures and information for accuracy and consistency across all documents. Work closely with the lender, CDC, or intermediary to ensure all requirements are met. Consider having an advisor from an SBA Resource Partner review the package for completeness before submission.

E. Confirming Eligibility Upfront

Submitting an application when the business, the project, or the requested use of funds is fundamentally ineligible for the chosen SBA program is an avoidable error.

Mitigation: Carefully review the specific eligibility criteria for the targeted loan program (7a, 504, Microloan) on the sba.gov website. Pay close attention to requirements regarding business type, size standards, eligible uses of funds, and any program-specific financial thresholds (like net worth/income for 504). Discuss eligibility frankly with the potential lending partner early in the conversation to confirm alignment before investing significant effort in the application.

F. Avoiding Predatory Lenders

The small business lending market can sometimes attract predatory actors. The SBA itself warns borrowers to be vigilant against lenders who impose unfair or abusive terms through deception or coercion. Falling victim to such practices can be financially devastating.

Mitigation: The most effective safeguard is to work exclusively with SBA-authorized lenders, CDCs, and intermediaries. Utilize official SBA resources like Lender Match and the lists of approved CDCs and Microloan intermediaries to find legitimate partners. Be wary of red flags highlighted by the SBA, such as :

Interest rates significantly higher than competitors'.

Excessive fees (e.g., more than 5% of the loan value).

Lack of clear disclosure of the Annual Percentage Rate (APR) and the full payment schedule.

Pressure tactics to accept a loan quickly.

Requests to sign blank forms or falsify information. If an offer seems too good to be true or raises concerns, survey competing offers and consider seeking advice from trusted financial advisors, accountants, or attorneys before signing any loan agreement. The existence of this explicit warning from the SBA underscores the reality of this risk and reinforces the value of using the SBA's vetted network of partners.

Your Strategic Path to SBA Financing

A. Recap of Key Qualification Steps

Successfully obtaining SBA-guaranteed financing requires a strategic and diligent approach. The pathway outlined by sba.gov resources involves several critical stages:

Confirm Foundational Eligibility: Verify that the business operates for profit, is based in the U.S., meets SBA size standards, and is an eligible type of enterprise.

Understand Program Options: Differentiate between the primary loan programs—7(a) for flexibility, 504 for fixed assets, Microloan for smaller needs—and select the one that best aligns with the specific funding purpose.

Assess Creditworthiness and Need: Evaluate the business's credit standing and ability to demonstrate repayment capacity. Understand and be prepared to address the "credit elsewhere" test, showing why SBA support is necessary.

Prepare a Compelling Application: Develop a robust business plan, compile accurate historical and projected financial statements, and gather all necessary supporting documentation.

Engage the Right Partner: Connect with the appropriate lending institution—an SBA 7(a) lender (via Lender Match or direct contact), a Certified Development Company (CDC) for 504 loans, or an approved Intermediary for Microloans.

Leverage Support Resources: Proactively utilize the free counseling and technical assistance offered by SBA Resource Partners (SBDCs, SCORE, WBCs) to strengthen the business plan, financials, and overall application package.

Navigate the Process: Work collaboratively with the chosen lending partner through the application submission, review, and closing stages.

B. Emphasis on Preparation and Partnership

Two themes resonate throughout the information available on sba.gov: the paramount importance of thorough preparation and the necessity of a strong partnership with the chosen lender, CDC, or intermediary. A well-documented, carefully planned request significantly enhances credibility and addresses lender concerns proactively. Building a transparent and collaborative relationship with the lending partner facilitates smoother navigation through the application and underwriting process. Furthermore, the availability of free, expert guidance from SBA Resource Partners represents a distinct strategic advantage that prudent business owners should actively incorporate into their preparation strategy.

C. Final Encouragement

The journey to securing an SBA loan demands effort, diligence, and attention to detail.

However, these programs represent a vital mechanism through which the federal government fulfills its mission to "aid, counsel, assist and protect" small businesses.

By understanding the requirements, preparing meticulously, choosing the right program and partner, and leveraging available support networks, business owners can significantly improve their prospects of accessing the capital needed to launch, sustain, grow, and ultimately strengthen their contribution to the American economy.

We can help you Navigate through the Small Business Financing maze.

The sooner you act, the more options you’ll have.

Schedule a consultation today and take the first step toward saving your business and your future.

Remember, more business debt isn’t the answer. A more effective business strategy is.

Click to setup an introduction meeting to discuss your situation and next best steps.

Bernarsky Advisors

Business Finance and Strategy Advice

Refinance. Restructure. Reorganize.

(See more of our articles about Business Finance and Strategy below…)

WHAT IS THE BEST AND SAFEST WAY FOR YOUR BUSINESS TO DEAL WITH HIGH BUSINESS DEBT PAYMENTS?

It is NOT by stopping ACH payments.

It is NOT by taking on another business loan.

It is NOT ALWAYS a Refinancing

It is NOT by entering into a debt settlement program.

Find out the BEST strategies to get your Business back to where it was

Setup a meeting with a business finance & strategy expert to discuss all of your options!

Read some other recent Business Finance and Business Strategy articles: